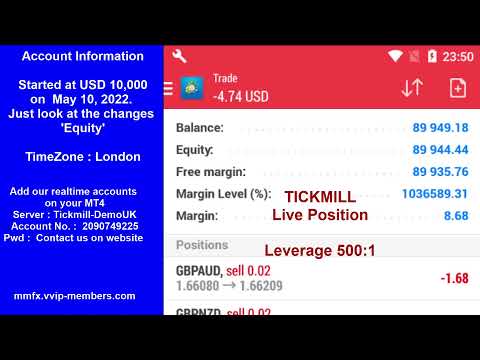

MoneyMaker FX Expert Advisor Robot Trading Account Live Streaming Visit website for more information.

https://mmfx.vvip-members.com/ Contact us

moneymakerfxea@gmail.com

MoneyMaker FX EA Trading Robot

MoneyMaker FX Expert Advisor Robot Trading Account Live Streaming Visit website for more information.

https://mmfx.vvip-members.com/ Contact us

moneymakerfxea@gmail.com

MoneyMaker FX EA Trading Robot

Forex EA Trading Robot

https://mmfx.vvip-members.com/ If your account balance is less than US$3,000, open an FBS Cent account via the link below.

https://fbs.com/cabinet/registration/trader/?ppu=9438088&account=stand&lang=en If your account balance is more than US$30,000, open an Tickmill Pro or VIP account via the link below.

https://secure.tickmill.com/?utm_campaign=ib_link&utm_content=IB79616275&utm_medium=%EA%B3%84%EC%A0%95+%EC%9C%A0%ED%98%95&utm_source=link&lp=https%3A%2F%2Ftickmill.com%2Fen%2Faccounts%2F

MoneyMaker FX EA Trading Robot

GBP/USD is virtually unchanged during the North American session on Monday amid hawkish comments by Atlanta’s Federal Reserve (Fed) President Raphael Bostic, even though United Kingdom (UK) data revealed that the economy grew at its fastest pace in one year.

Feed from Fxstreet.com

The People’s Bank of China (PBOC), China’s central bank, is responsible for setting the daily midpoint of the yuan (also known as renminbi or RMB). The PBOC follows a managed floating exchange rate system that allows the value of the yuan to fluctuate within a certain range, called a “band,” around a central reference rate, or “midpoint.” It’s currently at +/- 2%.

More strength again for the yuan, against a very weak US dollar. The mid-rate at 1.1534 today is the strongest for CNY since November 8 last year.

Previous close was 7.1636

PBOC injected 131bn yuan via 7-day reverse repos at 1.40%

This article was written by Eamonn Sheridan at www.forexlive.com.

Feed from Forexlive.com

The current price movements appear to be part of a range trading phase between 144.05 and 145.00. In the longer run, US Dollar (USD) appears to have moved into a range trading phase between 143.50 and 146.50 against Japanese Yen (JPY), UOB Group’s FX analysts Quek Ser Leang and Peter Chia note.

Feed from Fxstreet.com

UK BRC Shop Price Index for June 2025

This article was written by Eamonn Sheridan at www.forexlive.com.

Feed from Forexlive.com

New Zealand building permits for May 2025

+10.4% m/m

This article was written by Eamonn Sheridan at www.forexlive.com.

Feed from Forexlive.com

Australian final June 2025 manufacturing PMI 50.6, down from the flash reading and down from May.

Prelim is here:

Commentary from the report:

This article was written by Eamonn Sheridan at www.forexlive.com.

Feed from Forexlive.com

Japan plans to start extracting rare earth elements from the seabed near Minami-Torishima Island in fiscal 2025, beginning January 2026, according to Nikkei Asia (gated).

In brief:

The project, aimed at reducing dependence on China for critical minerals used in electric vehicles and electronics, was originally set for 2024 but was delayed due to a late pipe delivery.

This article was written by Eamonn Sheridan at www.forexlive.com.

Feed from Forexlive.com

The Pound Sterling (GBP) is soft and entering Monday’s NA session with a marginal 0.1% decline against the US Dollar (USD), trading just below last week’s multi-year highs, Scotiabank’s Chief FX Strategists Shaun Osborne and Eric Theoret report.

Feed from Fxstreet.com

The EUR/USD pair is trading sideways on Monday, consolidating near the multi-year highs, at 1.1750 reached last week.

Feed from Fxstreet.com

The USD Index (DXY) closed out June with a steep decline, hitting a new low for the year at 96.77, a level not seen since March 1, 2022. The index fell -2.67% in June, marking a clear shift in sentiment toward the U.S. dollar. All major currencies gained against the greenback this month, with the euro (EUR) and Swiss franc (CHF) posting the largest advances.

The EURUSD rose 3.86%, the biggest monthly gain among the majors. This move came despite the ECB delivering another rate cut, bringing its policy rate to 2.00%. Markets seem to believe the ECB is now prepared to pause after ten consecutive cuts, while the Fed remains stuck at 4.50%, delaying its own easing cycle. Traders increasingly expect the Fed to move earlier than previously anticipated, adding pressure on the dollar.

The USDCHF also posted strong losses, driven by flight-to-safety flows into the Swiss franc amid rising geopolitical tensions. Concerns that the U.S. could be drawn into the ongoing Iran–Israel conflict added to the CHF’s appeal.

Additional weakness in the dollar was fueled by growing political pressure. Donald Trump, in a surprising twist, sent a handwritten note to Fed Chair Powell accusing him of costing the country “millions” by delaying rate cuts, asserting that interest rates should already be at 1%. Trump has also hinted at replacing Powell, potentially as soon as January, raising questions about future monetary policy direction.

The market is now watching closely to see if the Fed bends under the pressure or stays the course. Either way, June’s sell-off in the dollar reflects everything from concerns about US deficits, to the expectation for sharply lower rates ahead, political interference, and mounting global risks.

The snapshot of the changes for the month showed:

In the US debt market in June yields have moved lower. A look at the yield changes along the interest rate curve:

In the US stock market for June, the major indices closed at record levels (for the second day in a row) to end the trading month. Gains were led by the NASDAQ index :

This article was written by Greg Michalowski at www.forexlive.com.

Feed from Forexlive.com

There are plenty of breathless headlines crossing about a 10.8% decline in the US dollar in “1H”.

Just for clarity that is NOT one hour as some folks seem to think. Sheesh, look at a chart!

Yes, the USD is awfully weak. Trump is debasing the dollar further with his threats against Fed independence, adding to the losses.

I posted yesterday, first thing,

And on Trump’s weekend dollar-debasement comments cutting the legs further from the dollar:

This article was written by Eamonn Sheridan at www.forexlive.com.

Feed from Forexlive.com

Morgan Stanley forecasts Brent crude will drop to around $60 per barrel by early 2026, citing easing geopolitical tensions — particularly between Israel and Iran — and a well-supplied market.

This article was written by Eamonn Sheridan at www.forexlive.com.

Feed from Forexlive.com