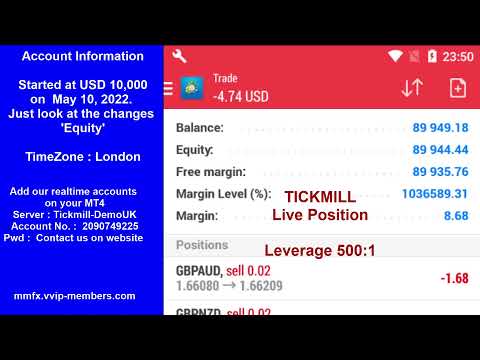

MoneyMaker FX Expert Advisor Robot Trading Account Live Streaming Visit website for more information.

https://mmfx.vvip-members.com/ Contact us

moneymakerfxea@gmail.com

MoneyMaker FX EA Trading Robot

MoneyMaker FX Expert Advisor Robot Trading Account Live Streaming Visit website for more information.

https://mmfx.vvip-members.com/ Contact us

moneymakerfxea@gmail.com

MoneyMaker FX EA Trading Robot

Forex EA Trading Robot

https://mmfx.vvip-members.com/ If your account balance is less than US$3,000, open an FBS Cent account via the link below.

https://fbs.com/cabinet/registration/trader/?ppu=9438088&account=stand&lang=en If your account balance is more than US$30,000, open an Tickmill Pro or VIP account via the link below.

https://secure.tickmill.com/?utm_campaign=ib_link&utm_content=IB79616275&utm_medium=%EA%B3%84%EC%A0%95+%EC%9C%A0%ED%98%95&utm_source=link&lp=https%3A%2F%2Ftickmill.com%2Fen%2Faccounts%2F

MoneyMaker FX EA Trading Robot

USD/CAD trades on the front foot on Friday despite a modest pullback in the US Dollar (USD), as weaker-than-expected Canadian Retail Sales data weighs on the Canadian Dollar (CAD). At the time of writing, the pair trades around 1.4170, its highest level since April 2025.

Feed from Fxstreet.com

Nordea analysts expect the Dollar to stay supported in coming months as the Federal Reserve maintains a relatively hawkish stance and US data remain firm. They argue that US growth and inflation dynamics justify higher yields versus peers, limiting Dollar downside.

Feed from Fxstreet.com

The coming week wraps up the month, the quarter, and the first half of the year. That combination often brings extra volatility as investors rebalance their portfolios. During the week of June 22–28, 2026, traders will be keeping a close eye on key economic data from Canada, Germany, the Eurozone, the UK, the US, Australia, and Japan, along with the People’s Bank of China’s policy decision. The highlights of the week will be the US PCE figures and the flash PMIs from S&P Global for Germany, the Eurozone, and the US. Note: During the coming week, new events may be… Read full author’s opinion and review in blog of #LiteFinance

Feed from Litefinance.com

Silver (XAG/USD) trades around $64.85 on Friday at the time of writing, down 1.31% on the day. The white metal remains under pressure for a third consecutive day as investors reassess the outlook for US monetary policy and developments in the Middle East.

Feed from Fxstreet.com

ING’s Francesco Pesole highlights that Andy Burnham’s by-election win paves his way to become UK Prime Minister, with betting markets expecting a transition by late summer. The absence of a political risk premium in Pound assets suggests investors see limited fiscal disruption.

Feed from Fxstreet.com

Deutsche Bank’s Galina Pozdnyakova, Jim Reid and Luke Templeman highlight that next week’s main macro focus will be global flash PMIs and several key inflation releases.

Feed from Fxstreet.com

Gold is supposed to be the asset you want when the world looks dangerous, which makes this week’s price action quietly remarkable.

Feed from Fxstreet.com

Nordea expects USD/JPY to remain high as wide US–Japan yield differentials persist and the Bank of Japan stays very accommodative. While some gradual BoJ normalization is anticipated, it is seen as too modest to materially weaken the Japanese Yen near term.

Feed from Fxstreet.com

The US Dollar Index (DXY) spent the back half of this week doing something most desks had written off six months ago: rallying on the prospect of a Federal Reserve (Fed) rate hike.

Feed from Fxstreet.com

Brent is back near $80 and West Texas Intermediate near $77, which means the Oil market has handed back almost the entire premium it built over nearly four months of open war with Iran.

Feed from Fxstreet.com

The textbook calls the Canadian Dollar a petro-currency, which means that with a Middle East war keeping Crude Oil bid, the Loonie should be holding its own.

Feed from Fxstreet.com

The Australian Dollar spent this week as a passenger in someone else’s trade.

Feed from Fxstreet.com