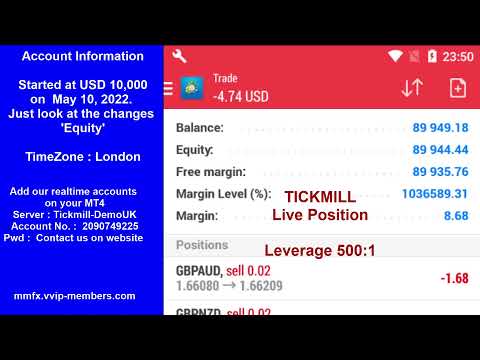

MoneyMaker FX Expert Advisor Robot Trading Account Live Streaming Visit website for more information.

https://mmfx.vvip-members.com/ Contact us

moneymakerfxea@gmail.com

MoneyMaker FX EA Trading Robot

MoneyMaker FX Expert Advisor Robot Trading Account Live Streaming Visit website for more information.

https://mmfx.vvip-members.com/ Contact us

moneymakerfxea@gmail.com

MoneyMaker FX EA Trading Robot

Forex EA Trading Robot

https://mmfx.vvip-members.com/ If your account balance is less than US$3,000, open an FBS Cent account via the link below.

https://fbs.com/cabinet/registration/trader/?ppu=9438088&account=stand&lang=en If your account balance is more than US$30,000, open an Tickmill Pro or VIP account via the link below.

https://secure.tickmill.com/?utm_campaign=ib_link&utm_content=IB79616275&utm_medium=%EA%B3%84%EC%A0%95+%EC%9C%A0%ED%98%95&utm_source=link&lp=https%3A%2F%2Ftickmill.com%2Fen%2Faccounts%2F

MoneyMaker FX EA Trading Robot

Gold price (XAU/USD) remained firm during Thursday’s North American session as the US Dollar remained solid following the release of robust jobs data, along with uncertainty about the latest tariffs imposed by Washington.

Feed from Fxstreet.com

The Swiss Franc (CHF) weakens against the US Dollar (USD) on Thursday, as the Greenback gains ground following stronger-than-expected US weekly jobless claims data, highlighting ongoing strength in the labor market.

Feed from Fxstreet.com

The stellar run for crypto continues:

No fresh news!

This article was written by Eamonn Sheridan at www.forexlive.com.

Feed from Forexlive.com

HSBC economists say that the European Central Bank is likely to proceed cautiously with further rate cuts, even though the euro’s recent strength could push inflation below the ECB’s 2% target, citing:

This article was written by Eamonn Sheridan at www.forexlive.com.

Feed from Forexlive.com

The European Commission is preparing to propose a floating price cap on Russian oil as part of its 18th sanctions package, aiming to adjust the cap in line with global oil price changes.

—

The background to this is that the original cap, set in 2022, bans tanker-based trade, insurance, and other services for Russian oil sold above the set limit. While some U.S. officials remain unconvinced about lowering the cap, momentum may build in Washington, especially as Trump signals a tougher stance on Russia and some U.S. senators express support for stricter measures.

Even if consensus is reached on the new price cap mechanism, Slovakia continues to oppose the broader sanctions package, citing concerns over the EU’s plan to fully phase out Russian energy imports by 2027. As EU sanctions require unanimous approval, this remains a key obstacle.

This article was written by Eamonn Sheridan at www.forexlive.com.

Feed from Forexlive.com

BNZ – BusinessNZ Performance of Manufacturing Index (PMI).

Still in contraction at 48.8 (a PMI reading above 50.0 indicates that manufacturing is generally expanding; below 50.0 that it is declining)

The long run average for the survey is 52.5.

BusinessNZ’s Director, Advocacy Catherine Beard:

BNZ’s Senior Economist Doug Steel:

—

Earlier this week the Reserve Bank of New Zealand left its cash rate target unchanged, and indicated that if inflaiton driops lwoer they’d lower rates:

Reserve Bank of New Zealand next meet on August 20.

This article was written by Eamonn Sheridan at www.forexlive.com.

Feed from Forexlive.com

The US Dollar reversed two daily drops in a row and charted acceptable gains on Thursday, following steady tensions on the trade front and another firm print from the weekly report on the US labour market.

Feed from Fxstreet.com

The Dow Jones Industrial Average (DJIA) rose on Thursday, paring back early-week losses following a fresh round of tariff threats from President Donald Trump.

Feed from Fxstreet.com

The Australian Dollar (AUD) is regaining confidence against the US Dollar (USD) on Thursday, with AUD/USD trading near 0.6580 at the time of writing. The latest move has been supported by a rebound in risk appetite and cautious sentiment surrounding the US Dollar.

Feed from Fxstreet.com

It’s a very light data agenda ahead for the session. New Zealand manufacturing PMI is the only item.

Earlier this week from NZ we had the RBNZ decision, on hold:

This article was written by Eamonn Sheridan at www.forexlive.com.

Feed from Forexlive.com

White House senior adviser Kevin Hassett criticised the Federal Reserve for not adequately explaining its past policy errors and raised concerns about its independence.

In a Fox Business interview, he said the next Fed Chair should consider reviewing the central bank’s overall size and structure. His remarks highlight increasing political pressure on the Fed and its decision-making.

This article was written by Eamonn Sheridan at www.forexlive.com.

Feed from Forexlive.com

Federal Reserve (Fed) Bank of San Francisco President Mary Daly hit newswires on Thursday, following up earlier comments from fellow Fed policymaker Christopher Waller, but taking a more measured approach to discussing the potential for near-term Fed rate cuts.

Feed from Fxstreet.com