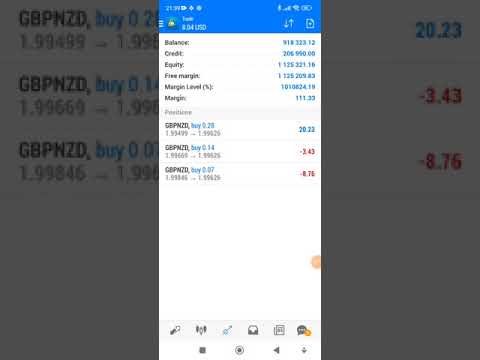

MoneyMaker FX Expert Advisor Robot Trading Account Live Streaming Visit website for more information.

https://mmfx.vvip-members.com/ Contact us

moneymakerfxea@gmail.com

MoneyMaker FX EA Trading Robot

MoneyMaker FX Expert Advisor Robot Trading Account Live Streaming Visit website for more information.

https://mmfx.vvip-members.com/ Contact us

moneymakerfxea@gmail.com

MoneyMaker FX EA Trading Robot

Forex EA Trading Robot

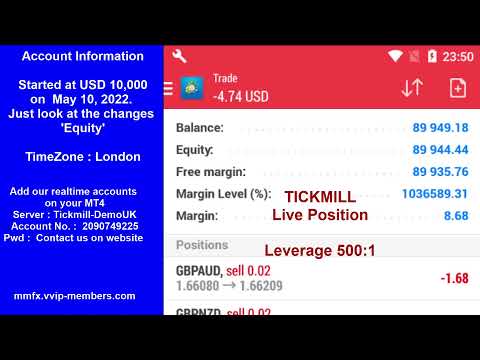

https://mmfx.vvip-members.com/ If your account balance is less than US$3,000, open an FBS Cent account via the link below.

https://fbs.com/cabinet/registration/trader/?ppu=9438088&account=stand&lang=en If your account balance is more than US$30,000, open an Tickmill Pro or VIP account via the link below.

https://secure.tickmill.com/?utm_campaign=ib_link&utm_content=IB79616275&utm_medium=%EA%B3%84%EC%A0%95+%EC%9C%A0%ED%98%95&utm_source=link&lp=https%3A%2F%2Ftickmill.com%2Fen%2Faccounts%2F

MoneyMaker FX EA Trading Robot

Fox Corp has agreed to acquire Roku Inc in a 22 billion USD deal, placing a major bet on digital television and ad-supported streaming. Fox gains direct access to over 100 million streaming households and a large pool of viewer data. For Fox, this is a chance to accelerate the growth of their own streaming […]

The post Fox Corp Acquires Roku for 22 Billion USD. What the Deal Means for FOXA Stock appeared first at RoboForex Blog.

Feed from Blog.roboforex.com

On 11 July 2024, the US Bureau of Labor Statistics released CPI data showing inflation down 0.1%. Within minutes, USD/JPY dropped nearly 400 pips. It was one of the sharpest single-day moves on that pair since late 2022. Many traders immediately suspected a Bank of Japan intervention, but the actual trigger was the inflation report. […]

The post Consumer Price Index (CPI): How It Works and Why Traders Watch It appeared first at RoboForex Blog.

Feed from Blog.roboforex.com

The Nasdaq 100 just closed out its best first half in years on a wave of AI enthusiasm, only to wobble in June. So what happens next?

Feed from Babypips.com

The 3 Tier London Breakout Indicator MT4 was created to help traders focus on one of the busiest forex sessions with a more structured approach. Instead of guessing where price may break, it highlights important breakout levels based on the London market opening. This allows traders to prepare their trades before volatility increases rather than […]

Feed from Forexmt4indicators.com

Markets enter the final week of June under elevated uncertainty, shaped by a hawkish Fed and renewed volatility in oil. The Fed held rates at 3.75% last week, but Chair Warsh’s commentary and the updated projections sent a clear message: rates will stay restrictive for as long as the inflation outlook demands. Oil added its […]

The post Market Week Ahead (June 22–26): Will the USD Pass June's Final Test? appeared first at RoboForex Blog.

Feed from Blog.roboforex.com

The All MACD Adaptive MTF Indicator MT4 was created to reduce that confusion. Instead of relying on a single timeframe, it combines the well-known MACD concept with adaptive calculations and multi-timeframe analysis. This helps traders see whether short-term momentum agrees with the bigger market direction before placing a trade. While no indicator can predict every […]

Feed from Forexmt4indicators.com

Silver just spent the first half of 2026 swinging from record highs to a sharp crash. So what happens next?

Feed from Babypips.com

To succeed in market trading you should learn to analyze and forecast price movements. The market price is influenced by a whole range of various factors, all of which we literally cannot know. A question emerges: in this case, how does forecasting become possible? This question is answered by one of the basic and most necessary types of market analysis — technical analysis.

The post What Is Technical Analysis? The Complete Beginner's Guide appeared first at RoboForex Blog.

Feed from Blog.roboforex.com

The IEA and Goldman Sachs expect significant oil market surpluses in 2027. Combined with the reopening of the Strait of Hormuz, rising Iranian and Russian exports, and declining demand in Asia and Europe, this factor is pushing Brent prices lower. Let’s analyze the situation and develop a trading plan. Major Takeaways The US dollar is putting pressure on Brent. Exports from Iran and Russia are growing rapidly. The IEA and Goldman Sachs expect a global oil market surplus in 2027. Profits can be taken if Brent drops to $70. Weekly Fundamental Forecast for Oil During the conflict in the Middle… Read full author’s opinion and review in blog of #LiteFinance

Feed from Litefinance.com

What’s next for gold in the second half of 2026? After record highs and a sharp pullback, gold’s next big move remains an open question.

Feed from Babypips.com

What is AI cryptocurrency? This is a question many people ask as the worlds of artificial intelligence and blockchain continue to converge. Unlike Bitcoin, which primarily serves as a store of value, AI cryptocurrencies combine AI and blockchain technology to create tokens with real-world utility. They can be used to pay for computing resources, access AI models and neural networks, and power decentralized applications and services. The AI crypto sector is already valued at more than $26 billion, while global investment in artificial intelligence has surpassed $140 billion. Some AI-related crypto tokens have delivered annual gains of 200% or more…. Read full author’s opinion and review in blog of #LiteFinance

Feed from Litefinance.com