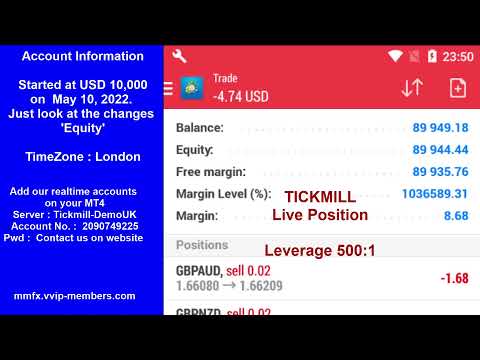

MoneyMaker FX Expert Advisor Robot Trading Account Live Streaming Visit website for more information.

https://mmfx.vvip-members.com/ Contact us

moneymakerfxea@gmail.com

MoneyMaker FX EA Trading Robot

MoneyMaker FX Expert Advisor Robot Trading Account Live Streaming Visit website for more information.

https://mmfx.vvip-members.com/ Contact us

moneymakerfxea@gmail.com

MoneyMaker FX EA Trading Robot

Forex EA Trading Robot

https://mmfx.vvip-members.com/ If your account balance is less than US$3,000, open an FBS Cent account via the link below.

https://fbs.com/cabinet/registration/trader/?ppu=9438088&account=stand&lang=en If your account balance is more than US$30,000, open an Tickmill Pro or VIP account via the link below.

https://secure.tickmill.com/?utm_campaign=ib_link&utm_content=IB79616275&utm_medium=%EA%B3%84%EC%A0%95+%EC%9C%A0%ED%98%95&utm_source=link&lp=https%3A%2F%2Ftickmill.com%2Fen%2Faccounts%2F

MoneyMaker FX EA Trading Robot

The combination of VWAP (Volume Weighted Average Price) Bands with the Kolier SuperTrend indicator has emerged as a robust strategy in forex trading, offering traders a comprehensive approach to analyzing market trends and potential trading opportunities. VWAP Bands are instrumental in providing traders with a nuanced view of price movements, reflecting average prices weighted by […]

Feed from Forexmt4indicators.com

Silver ended its two-day losing streak yet finished the week with losses of more than 4%, as investors booked profits in the precious metal space.

Feed from Fxstreet.com

Imagine the price movement of an asset like a river. Sometimes, the river flows turbulently, with unpredictable currents. Other times, it settles into a calm channel, with clear boundaries. Trend channels represent these well-defined pathways in the market, where prices tend to fluctuate within a specific range. Identifying these channels is crucial for technical analysis, […]

Feed from Forexmt4indicators.com

The Japanese yen found itself at the top of the daily leaderboard thanks to calls for BOJ tightening and a big return in broad negative risk sentiment.

Feed from Babypips.com

As the North American session begins, the AUD is the strongest and the JPY is the weakest. That combination reverses what has been more of a familiar theme with the AUD (or NZD) weakest and the JPY the strongest. Not surprisingly, there is a rebound in US stocks in the pre-market which is helping the reversal. The Nasdaq is up 200 points (currently) in premarket futures trading. That reverses the -160 point decline from yesterday. Nevertheless, the major US indices are on pace for a declines this week.

The unwind of the USDJPY and the so called “carry trade” where some investors borrow the yen at low rates to invest in USD assets (or other countries assets) for better returns,has been an excuse for the flow of funds out of some assets and into others.Having said that, the Nikkei 225 had its worst day since 2021 this week. Bitcoin, oil, silver, copper and even gold fell this week. So there may be selling of the USD and liquidation in things like the US stocks but it seems to be going into cash. It will be interested how this story unwinds.

Of course, when you have moves like we have had this week especially out of assets like the Magnificent 7, it is always fun to find the “reason” (i.e. carry trade unwind), but it just can be “taking profit” and yes parking in cash or money market for a while. The Fed does meet next week, and with 2% or thereabout growth in the 1H of 2024, it may make it hard to cut. So parking funds for a while and buy a dip might be a sound idea.

BTW, The BOJ does meet next week,and the market is pricing in a 65% chance for a 10 basis point rise in rates. The US Fed also meets and the focus by the markets is on the central bank starting the cuts in September.

Today’s data, may help the Fed with that decision as the favored measure of inflation (the core PCE) will be released at 8:30 AM ET. A review of the economic data to be released today, will be highlighted by the PCE data along with the University of Michigan consumer sentiment (final) at 10 AM ET. :

A snapshot of the other markets as the North American session begins shows:

In the premarket, the snapshot of the major indices are trading higher.

European stock indices are trading mostly higher. For the week the indices are also mixed:

Shares in the Asian Pacific markets closed lower:.

Looking at the US debt market, yields are trading mixed:

Looking at the treasury yield curve,

In the European debt market, the benchmark 10-year yields are lower:

This article was written by Greg Michalowski at www.forexlive.com.

Feed from Forexlive.com

Market correlations fell in & out of sync & broad risk vibes were soured as traders juggled several major market narratives, including fears of a slowdown in China.

Feed from Babypips.com

The US stocks have closed the week with gains on the day.

The S&P and the Nasdaq remain lower on the week. The Dow and the small-cap Russell 2000 closed higher with the Russell 2000 the best performer on the rotation on hopes lower rates would help those companies going forward.

The final numbers are showing:

The small-cap Russell 2000 rose to 37.08 points or 1.67% at 2260.06.

For the trading week:

Next week is a huge week with Amazon, Apple, Meta Platforms, and Microsoft all scheduled to release earnings.

Today:

For a list of the other companies scheduled to release can be found HERE. Of course the Fed interest rate decision on Wednesday will also be a key event. The week will also end with the US jobs report on Friday (177K estimate with the unemployment rate at 4.1%).

This article was written by Greg Michalowski at www.forexlive.com.

Feed from Forexlive.com

Yesterday morning, the CNY was able to take advantage of the JPY’s strength against the US Dollar and also appreciated significantly against the greenback.

Feed from Fxstreet.com

I posted this during the Asian time zone, repeating it here. Before I do, check this out:

—

Due at 0830 US Eastern time, the Core PCE data is the focus. You can see the median estimates below in the table.

The ranges (why these are important is explained below) of estimates are:

Core PCE Price Index m/m

and for the y/y

***

Why is knowledge of such ranges important?

Data results that fall outside of market low and high expectations tend to move markets more significantly for several reasons:

Surprise Factor: Markets often price in expectations based on forecasts and previous trends. When data significantly deviates from these expectations, it creates a surprise effect. This can lead to rapid revaluation of assets as investors and traders reassess their positions based on the new information.

Psychological Impact: Investors and traders are influenced by psychological factors. Extreme data points can evoke strong emotional reactions, leading to overreactions in the market. This can amplify market movements, especially in the short term.

Risk Reassessment: Unexpected data can lead to a reassessment of risk. If data significantly underperforms or outperforms expectations, it can change the perceived risk of certain investments. For instance, better-than-expected economic data may reduce the perceived risk of investing in equities, leading to a market rally.

Triggering of Automated Trading: In today’s markets, a significant portion of trading is done by algorithms. These automated systems often have pre-set conditions or thresholds that, when triggered by unexpected data, can lead to large-scale buying or selling.

Impact on Monetary and Fiscal Policies: Data that is significantly off from expectations can influence the policies of central banks and governments. For example, in the case of the inflation data due today, weaker than expected will fuel speculation of nearer and larger Federal Open Market Committee (FOMC) rate cuts. A stronger (i.e. higher) CPI report will diminish such expectations.

Liquidity and Market Depth: In some cases, extreme data points can affect market liquidity. If the data is unexpected enough, it might lead to a temporary imbalance in buyers and sellers, causing larger market moves until a new equilibrium is found.

Chain Reactions and Correlations: Financial markets are interconnected. A significant move in one market or asset class due to unexpected data can lead to correlated moves in other markets, amplifying the overall market impact.

This article was written by Eamonn Sheridan at www.forexlive.com.

Feed from Forexlive.com

For most of the week, the flow of funds sent the JPY and CHF higher on flight to safety flows. The AUD (and NZD) lower as risk off sentiment dominated on the back of slowdown in China, lower commodities and stocks moving lower.

Today saw a reversal of some of those trends.

For the day, the AUDSD is the strongest of the majors. The CHF is ending as the weakest. The JPY is ending the day mixed. The USD which was mixed for a lot of the week is ending the week with the same fortunes today.

Stocks moved higher in both Europe and the US today.

The major European indices bounced back in trading today with all the indices higher.

For the trading week, most of the indices were higher except Italy’s FTSE MIB

The final numbers in the US closed the day with gains across the board.

For the trading week, the results were mixed with the Dow up for the 4th consecutive week. The Russell 2000 was up for the 3rd week.. The S&P and the Nasdaq were down for the 2nd consecutive week. Next week will be influenced by a slew of earnings highlighted by Microsoft, Apple, Amazon and Amazon amongst other large cap titans in various industries.

US yields are closing the day near lows across the yield curve:

For the trading week:

The 2-10 year rose by 8.3 basis points for the week to -19.4 basis pointe. The 2-30 year spread is ending positive by 6.7 basis points.

Fundamentally today, the PCE data was consistent with the PCE data from the GDP data yesterday.

The core PCE moved up by 0.188% (rounded to 0.2%. The YoY rose by 2.6%. The was unchanged from last month. The headline PCE rose of 0.1% (revised higher) with the YoY dipping to 2.5% from 2.6%.

The Michigan consumer survey data was mixed with the sentiment moving higher vs the preliminary, the current conditions lower and the expectations higher . Inflation results were more or less as expected and close to last months levels.

IN addition to the parade of earnings, the Fed, the Bank of England and the Bank of Japan will announce interest rate decision. The US jobs report will be released on Friday. Australia and EU CPI will be released. China PMI will be released as well.

Thank you for the support.this week. Wishing you all a great weekend (PS enjoy the Olympics).

This article was written by Greg Michalowski at www.forexlive.com.

Feed from Forexlive.com

The AUD/USD pair remains steady above the immediate support of 0.6520 in Friday’s New York session after the release of the mixed United States (US) Personal Consumption Expenditure Inflation (PCE) report for June.

Feed from Fxstreet.com