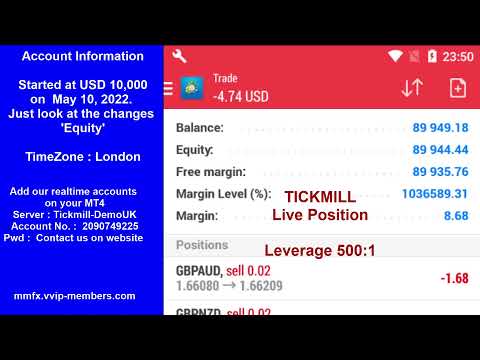

MoneyMaker FX Expert Advisor 機器人交易賬戶實時流媒體訪問網站了解更多信息。

https://mmfx.vvip-members.com/ 聯繫我們

moneymakerfxea@gmail.com

MoneyMaker FX EA 交易機器人

MoneyMaker FX Expert Advisor 機器人交易賬戶實時流媒體訪問網站了解更多信息。

https://mmfx.vvip-members.com/ 聯繫我們

moneymakerfxea@gmail.com

MoneyMaker FX EA 交易機器人

外匯 EA 交易機器人

https://mmfx.vvip-members.com/ 如果您的賬戶餘額低於 3,000 美元,請通過以下鏈接開設 FBS Cent 賬戶。

https://fbs.com/cabinet/registration/trader/?ppu=9438088&account=stand&lang=en 如果您的賬戶餘額超過 30,000 美元,請通過以下鏈接開設 Tickmill Pro 或 VIP 賬戶。

https://secure.tickmill.com/?utm_campaign=ib_link&utm_content=IB79616275&utm_medium=%EA%B3%84%EC%A0%95+%EC%9C%A0%ED%98%95&utm_source=link&lp=https%3A%2F %2Ftickmill.com%2Fen%2Faccounts%2F

MoneyMaker FX EA 交易機器人

Crude Oil tries to hold ground and orbits around the $70.00 level on Tuesday. The pressure on Oil’s price comes from markets repricing the US Federal Reserve (Fed) interest rate cut projections in the near future. With decreasing odds of an aggressive

來自 Fxstreet.com 的提要

Markets:

It’s been

another slow session as the lack of key economic releases and limited news flow

kept the price action pretty rangebound.

The US

Dollar continues to get some support from higher Treasury yields and if the

recent days is something to go by, we might see some more legs higher in the US

session.

Gold erased

all of the yesterdays’ decline and it’s now trading right near the all-time

high. It’s been ignoring the rise in real yields, so it will be interesting to

see who gives in.

In the equity

markets, we continue to see some consolidation around the highs as the markets

are probably looking for catalysts to push into new highs and for now are

getting pressures by higher yields.

Unfortunately,

we have to wait until Thursday to get some market moving data with the releases

of the Flash US PMIs and the US Jobless Claims.

For now, it’s

more about capital preservation until we get to one of the most important

events of the year in November, that is the US election. There’s a good

argument that the markets have been already positioning into a Trump victory.

Time will

tell.

This article was written by Giuseppe Dellamotta at www.forexlive.com.

Feed from Forexlive.com

![Hindustan Unilever Elliott Wave technical analysis [Video]](https://i0.wp.com/mmfx.vvip-members.com/wp-content/uploads/2024/10/hindustan-unilever-elliott-wave-technical-analysis-video.png?resize=400%2C250&ssl=1)

Function: Larger Degree Trend Higher (Intermediate degree, orange) Mode: Motive Structure: Impulse Position: Minute Wave ((iii)) Navy Details: Minute Wave ((iii)) Navy is progressing higher within Minor Wave 3 Grey of Intermediate Wave (5) Orange against 2425.

來自 Fxstreet.com 的提要

For months I’ve highlighted the drag from commodity prices and now we have Canadian CPI running at 1.5% y/y. That will continue for a couple more months with WTI running at $71 but at some point the commodity drag on inflation becomes a boost. That’s why core inflation is so key right now.

This article was written by Adam Button at www.forexlive.com.

Feed from Forexlive.com

Aventus, a leading provider of enterprise blockchain

solutions and parachain on Polkadot, today confirms the launch of Aventus 2.0,

an evolution of the Aventus Network aimed at establishing a stronger foundation

for long-term growth and value capture.

The update introduces several strategic initiatives designed

to enhance network performance and stakeholder utility, including increasing

transaction volume and overall network usage, expanding the ecosystem through

successful partnerships with Layer 3 appchains, enhancing token holder

engagement via a liquidity mining program, and reducing token supply via a burn

mechanism.

The vision for Aventus 2.0 was developed by MVP Workshop, a

Blockchain Product Research & Development Studio who designed Polygon Edge

and Astar Network, in collaboration with Scytale Digital and the Aventus

Services team.

Following the approval of a community governance proposal in

which AVT token holders voted in favour of executing this vision, the Aventus

Services team will implement the Aventus 2.0 plan over the next four months.

This process underscores Aventus’s commitment to stakeholder-driven

decision-making, ensuring that major network decisions are made through

community consensus.

Aventus 2.0 comprises three main components:

Alan Vey, Founder at Aventus, commented: “Aventus 2.0 builds

on important learnings from existing Aventus Network clients as well as the

invaluable expertise of our partners at MVP Workshop & Scytale Digital, and

represents a significant milestone in our journey to enhance the Aventus

Network’s capabilities and deliver greater value to stakeholders.”

The appchain model is already seeing traction, with existing

users of the Aventus Network having recently launched their own Aventus Layer 3

appchains.

Barry Helfrich, CIO at Enigmatic Smile, adds: “We needed the

Voucher Ledger solution to be secure, fast and stable enough to process the

discounts collected by hundreds of millions of users in our rewards ecosystem —

no small feat, but Aventus has helped us build such a solution. The team has

been helpful, professional and responsive throughout the process. We’re looking

forward to continuing our long-standing relationship with them.”

The updated network will provide enhanced functionality and

improved user experiences, positioning the Aventus Network as a trusted leader

in enterprise blockchain solutions and key contributor to enterprise use cases

within the Polkadot ecosystem.

About Aventus

Aventus (https://www.aventus.io/) transforms how customers

create trust and unlock growth, crafting pioneering Web3 solutions for brands,

from creating more connected, integrated experiences to enhancing traceability,

transparency, and product authentication. Founded in 2020, Aventus is the only

trusted digital product extension platform that provides a secure and reliable

Web3 environment for customers to launch market-leading programs and product

activations.

With deep industry expertise and a strong understanding of

enterprise needs, Aventus delivers one the best feature sets of Web3 with the

familiarity of Web2, driving significant brand reputation, trust, and

enterprise growth for its customers. Its production-ready, end-to-end

Blockchain-as-a-Service software is modular, scalable, and interoperable,

giving clients the flexibility they need to respond to rapidly evolving market

opportunities.

This article was written by FL Contributors at www.forexlive.com.

Feed from Forexlive.com

Strategy: 3/12 Tunnel The 3/12 Tunnel is a trend-following strategy. This straightforward approach utilizes 3 moving averages has undergone extensive backtesting by our team, demonstrating a winning ratio between 70% and 80%. Recommended Timeframe This strategy is adaptable to various timeframes, including H1, H4, and Daily. Although it can be applied to timeframes lower than […]

來自 Forexmt4indicators.com 的提要

Feed from Investing.com

Chinese oil refineries processed 58.7 million tons of crude oil in September, Commerzbank’s commodity analyst Carsten Fritsch notes.

來自 Fxstreet.com 的提要

EUR/USD trade has been a little choppy, within a limited range, so far on the session, Scotiabank’s Chief FX Strategist Shaun Osborne notes.

來自 Fxstreet.com 的提要

European indices are also all in negative territory, with the DAX also down by 0.1% after a decent open earlier. Other major indices in the region are down some 0.6% to 0.8% with the negative mood also reflected in US futures. S&P 500 futures are down 0.5% with Nasdaq futures down 0.6% currently.

In the bigger picture, it’s a case of shaving some off the top for equities. And investors can look to the bond market as a likely reason for that. 10-year Treasury yields are up again today, touching 4.21% currently.

The technical focus here is starting to get traders to stand up and take notice. And that means broader markets are also going to have to pay attention to that too.

This article was written by Justin Low at www.forexlive.com.

Feed from Forexlive.com

Goat Funded

Trader (GFT), a prop firm offering retail investors access to accounts up to

$800,000, has just announced the addition of cTrader, Spotware’s popular

trading tool, to its lineup of investment platforms. This is the latest product

introduced by GFT in recent months, following the addition of TradeLocker and

the farewell to MetaTrader.

Prop Firm Goat Funded

Trader Unveils New Platform: cTrader Added to the Mix

In recent

days, Goat Funded Trader has been teasing its clients on social media with

hints of a “big announcement.” Some traders correctly guessed that

GFT was introducing a new platform, cTrader from Spotware. To celebrate this

update, the prop firm is also offering discounts on its challenges using the

code CTRADER.

📢 cTrader IS NOW LIVE 📢The news everyone was waiting for 🔥To celebrate the introduction of this new platformGFT offers a 25% OFF on all Challenges!✅Available for 72 hours only🎟️Code: CTRADERDon’t miss the chance and join us now pic.twitter.com/5vXGmEDyGH

— Goat Funded Trader (@GoatFunded) October 21, 2024

After

moving away from MetaQuotes’ trading platforms twice this year, GFT has been on

the hunt for alternative solutions to offer its traders. In response, the

company first introduced TradeLocker access in July, and then considered

launching cTrader in August.

“We

heard you want cTrader as well. Recently we introduced TradeLocker. Should we

add cTrader?” CEO Edoardo Dalla Torre asked in September. Two months after

posing this question, the prop firm is now delivering on its clients’

expectations by implementing the new platform.

GFT was

among the first firms to drop MetaQuotes’ platform in February 2024 due to

licensing issues. Although the company briefly brought back the popular trading

tools, the return was short-lived.

cTrader Gains Popularity

Among Prop Firms and Traders

cTrader,

alongside TradeLocker and MatchTrader, has become a popular choice for prop

firms transitioning away from MetaTrader. In recent months, The Funded Trader

and MyFundedFX have also added the platform to their offerings.

According

to PropFirmMatch data, at least a dozen verified and trader-recommended prop

firms currently use cTrader. These include FTMO, Fintokei, Funding Pips, and

Lark Funding. Fintokei recently boasted that it paid out over €4 million to

traders in just the first eight months of this year.

Meanwhile,

Spotware, the company behind cTrader, has released version 5.0.22 of its

desktop application. The latest update introduces a new feature and addresses

several issues to improve user experience and overall performance.

This article was written by Damian Chmiel at www.financemagnates.com.

Feed from Financemagnates.com

The Canadian Dollar (CAD) has had a minor reprieve this morning as it holds little changed on the session but some 20 ticks above yesterday’s low against the USD in the mid-1.38s, Scotiabank’s Chief FX Strategist Shaun Osborne notes.

來自 Fxstreet.com 的提要